Everybody’s Working for the Weekend: The State of the U.S. Labor Market

Everyone’s watching, to see what you will do

Everyone’s looking at you, oh

Everyone’s wondering, will you come out tonight

Everyone’s trying to get it right, get it right

Everybody’s working for the weekend

“Everybody’s Working for the Weekend”, Loverboy

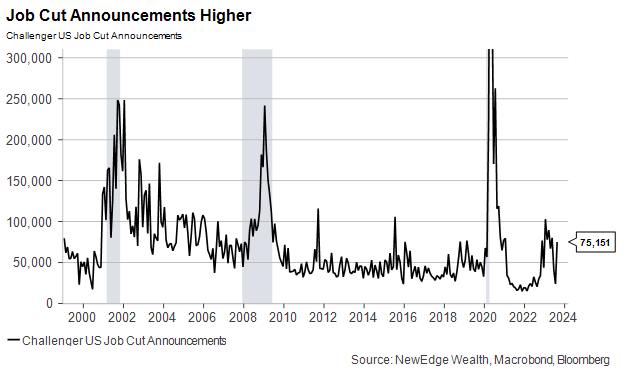

In honor of Labor Day weekend, we will look at the state of the U.S. labor market (quickly and with charts at the end, so that you can get back to your beach reading).

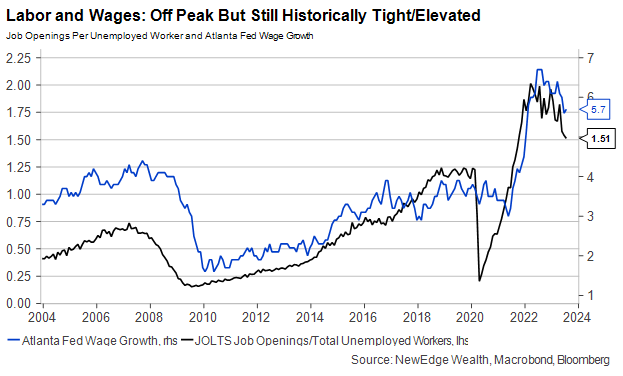

The summary is that the U.S. labor market remains resilient and historically tight. There have been signs of easing coming out of the post-pandemic pronounced tightness, but this easing has been more in the flavor of normalization to pre-pandemic levels versus distinct weakening.

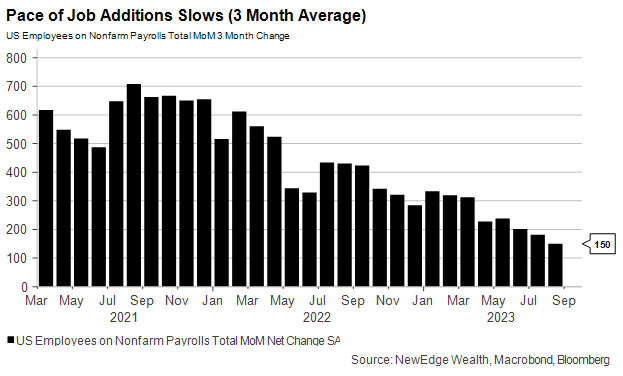

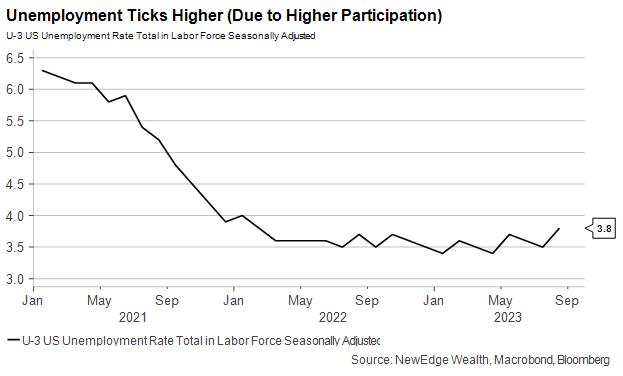

There has been a Goldilocks nature of recent employment data, with easing in softer and secondary data, like Job Openings, and moderation in the pace of wage gains (some measures show more moderation than others), all while measures of absolute employment, like Nonfarm Payrolls, remain relatively robust. Note, there has been a marked slowdown in the pace of job gains in recent months, but while the Unemployment Rate did tick up in Friday’s Jobs report, it was likely attributed to the higher labor force participation rate.

This Goldilocks data is effectively the Federal Reserve’s wished-for “golden path”, with the boil of inflationary, above-trend wage growth being reduced without causing a large jump in unemployed workers.

Of course, the phrase “be careful what you wish for” should always be an öhrwurm/earworm for investors (at least to drown out those classic 1981 Loverboy lyrics likely now stuck in your head… sorry about that). The Fed and markets are wishing for easing in order to quell inflation, but what if there is too much easing? The critical question from this juncture will be if the recent easing stops at golden normalization, or if it will continue and build into a more pernicious and painful softening in the jobs market.

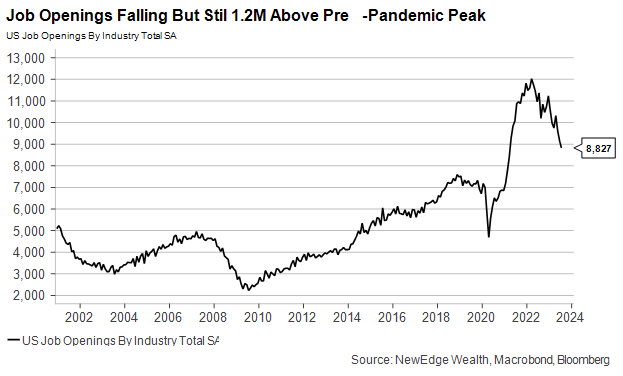

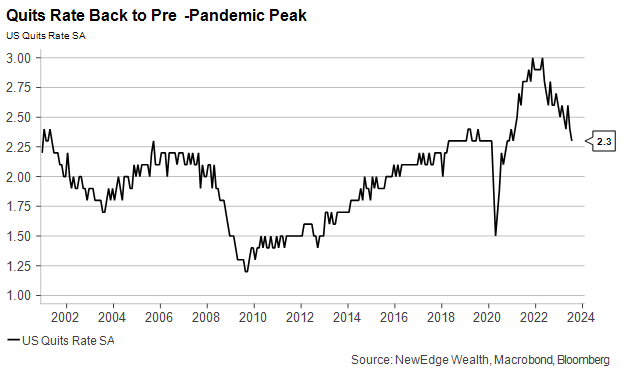

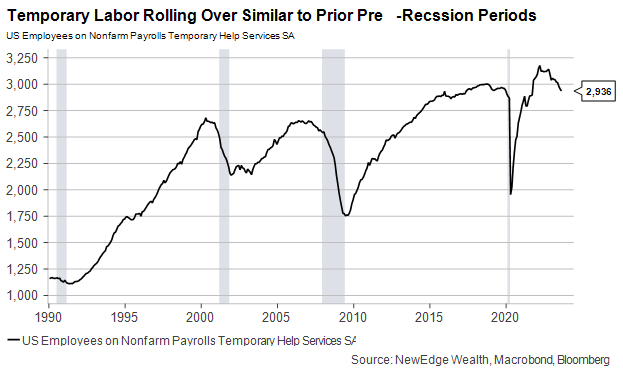

Many of the statistics being currently lauded as soft-landing evidence are also considered leading indicators for lagging labor statistics, like the Unemployment Rate. This means that softness in things like Job Openings, Quits, and Temporary Employment, are often seen as an early sign of brewing broader labor and economic weakness. For now, these leading labor indicators have simply been normalizing, but if recent downtrends/easing continue, calls for economic weakness will likely amplify.

The key difference in considering this data today compared to prior cycles, is that all of this (and most other!) data is still wildly distorted by pandemic disruptions. This is why so many economic models have struggled in 2022 and 2023, forecasting a recession that simply hasn’t materialized. The models have not been able to differentiate between the slowing/deterioration in data from benign normalization post-pandemic and from the out-right weakening typically seen before a recession.

For now, this Goldilocks path buys the Fed time to be patient and likely not hike rates in September (Fed Funds Futures show just a 7% chance of a September hike). We think November is still a “live meeting”, meaning another hike is still on the table (futures show a 38% chance of November hike), if only because the Fed itself has one more hike penciled in for 2023 in its Dot Plot. Of course, this “data dependent” Fed will remain highly sensitive to incoming data, so any hot or cold jobs and/or inflation report could easily swing the Fed’s decision.

We have seen both bonds and stocks rally (bond yields down, stock prices up) on this string of Goldilocks data. We think resilient economic data keeps a floor under interest rates, with a continued steep drop in rates across the curve reliant on seeing more pronounced economic weakness (pricing in both a swift start to Fed rate cuts on the short end and a flight to safety on the long end). Without a steep rise in interest rates, for now equities can fully enjoy the boost they are experiencing from a recent increase in earnings forecasts. The “be careful what you wish for” scenario is most critical for equities, where if we do see evidence of labor normalization morphing into weakness, this beneficial earnings revision upcycle will likely be stalled as expectations for a weaker economy are baked into forecasts.

Enjoy your Labor Day Weekend and labor charts below!

All charts as of 9/1/23

Top Points of the Week

By Connor Finnigan

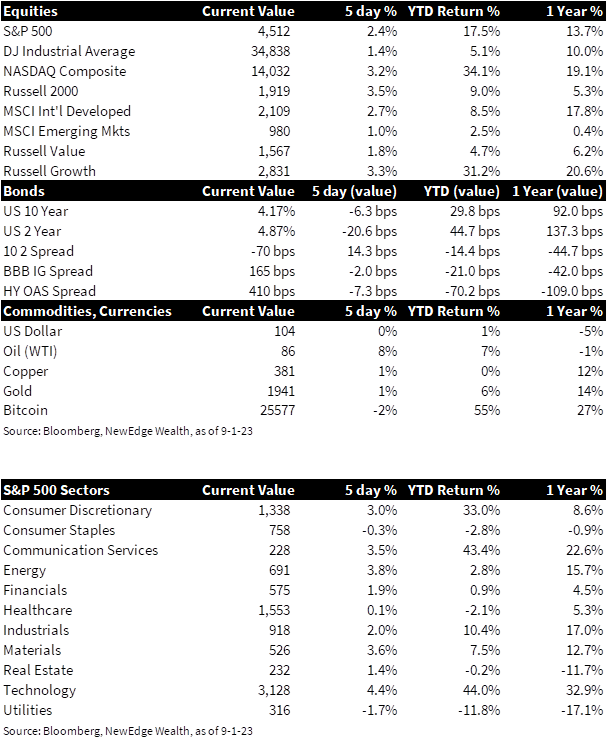

1. Economic data lifts US equities to finish the week – US Equities seem to have rebounded this week after a weak month. The S&P 500 is up 1.8%, Dow is up 1%, and the Nasdaq is up over 2% on the week. The resilience of economic data and markets has been a trend we have seen throughout this year. Although there is a goldilocks scenario forming in the US, troubles still lurk overseas with demand for Chinese services and factory output, and rising inflation in the Eurozone.

2. US crude oil futures climb over $2 a barrel – Through the month of August, crude oil continuous contracts have seen a 5.30% increase. US crude oil prices gained more than $2 on Thursday, which marks the third consecutive month of a price increase. These price jumps can be attributed to expectations that OPEC+ will continue to cut oil barrel production through the end of 2023. It will be interesting to see how these price increases will affect US consumers, who have remained resilient throughout the year.

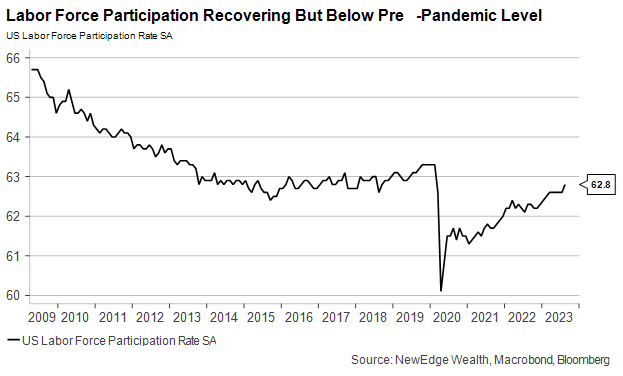

3. August jobs report comes in better than expected – The August jobs number was a very healthy report and added more jobs than expected. The jobs market grew by 187k, which was above the Dow Jones estimate of 170k. The unemployment rate rose to 3.8% which is up significantly from July’s print and marks the highest level since February 2022. This increase came from the labor force participation rate rising to 62.8%, the highest reading since February 2020. The report can be thought of as a win for the Fed and gets them closer to a Goldilocks scenario of a soft landing.

4. July JOLTS report come in weaker than expected – The July JOLTS report on Wednesday showed job openings falling 338k to 8.827 million which is the lowest level since March 2021. We interpret this as a dovish data point that the labor market is showing signs of easing. Labor market conditions still remain tight, with 1.51 job openings for every unemployed person in July, compared to 1.54 in June. However, it is important to note that quits dropped 253k to 3.549 million while layoffs remained unchanged. A decrease in the number of quits indicates that workers are less confident about the labor market.

5. US 2Q 2023 GDP revised downward – US Q2 GDP was revised to 2.1% from 2.4% earlier this week. Economists had expected that GDP for the second quarter would be unrevised. GDP is expanding at a pace well above what Fed officials regard as the non-inflationary growth rate of around 1.8%. The Fed has been aggressively increasing interest rates to combat inflation and slow demand, although the economy is remaining quite resilient.

6. July PCE data release: the US consumer remains resilient – The Personal Consumption Expenditures (PCE) index, which is the Fed’s preferred measure of inflation, showed that headline prices increased 0.2% on a monthly basis and 3.3% annually. Core PCE, which strips out the more volatile areas of food and energy, showed prices increased 0.2% from the month before and 4.2% on an annual basis. Despite higher prices and lower personal income, consumers are continuing to spend which is not what the Fed wants to see in a high inflation environment.

7. Story of weak demand in China – China continues its struggles of declining factory output due to lower consumer demand. Chinese Manufacturing PMI in August was up month over month, but still in contractionary territory for the fifth straight month. Chinese Services PMI in August came in below expectations, with the lowest reading since January and far below pre-pandemic levels, although still in expansionary territory.

8. August Eurozone CPI comes in hotter than expected – Inflation across the 20 countries in the Eurozone remained unchanged. Headline CPI came in higher than expected at 5.3% on an annual basis. Core CPI dropped from July’s 5.5% reading to 5.3%, which was as expected. The report prompted financial markets to revise their view on the chance of a September rate hike to 33% from around 50% earlier this week and indicates that there is more work to be done by the European Central Bank.

9. Earnings stock highlight: Broadcom – Broadcom (AVGO) reported a healthy quarter with modest beats on both top and bottom lines. The company is seeing margin expansion and healthy free cash flow generation. The AI demand is real – advanced chip revenues are growing at 20% year over year. The stock is pretty much flat on the day after being up 4% yesterday to down 4% this morning after guiding slightly lower.

10. Incoming data next week – Markets are closed on Monday for Labor Day, but Wednesday we get some important data points including the U.S. trade deficit report, both ISM and S&P Services PMI report, and the Fed Beige Book. The rest of the week is filled with Fed speakers which will give us insight into their thought processes for the next FOMC meeting.

IMPORTANT DISCLOSURES

Abbreviations/Definitions: AI: artificial intelligence; Beige Book: Summary of Commentary on Current Economic Conditions by Federal Reserve District is a report is published eight times per year, where each Federal Reserve Bank summarizes anecdotal information on current economic conditions in its District; Core CPI: measures the changes in the price of goods and services, excluding food and energy; Core PCE: personal consumption expenditures prices excluding food and energy prices; Fed Fund Futures: derivatives that measure expectations of Fed policy; GDP: gross domestic product; Headline CPI: the raw inflation figure reported through CPI that calculates the cost to purchase a fixed basket of goods to determine how much inflation is occurring in the broad economy; ISM Manufacturing PMI: Institute for Supply Management Purchasing Managers Index; JOLTS: Job Openings and Labor Turnover Survey; Organization of the Petroleum Exporting Countries (OPEC) – The Organization of the Petroleum Exporting Countries is a cartel consisting of 13 of the world’s major oil-exporting nations that aims to regulate the supply of oil in order to set the price on the world market; OPEC+: an OPEC coalition with 10 of the world’s major non-OPEC oil-exporting nations that represents around 40% of world oil production and its main objective is to regulate the supply of oil to the world market; PCE: personal consumption expenditures; PMI: Purchasing Managers’ Index.

Index Information: All returns represent total return for stated period. S&P 500 is a total return index that reflects both changes in the prices of stocks in the S&P 500 Index as well as the reinvestment of the dividend income from its underlying stocks. Dow Jones Industrial Average (DJ Industrial Average) is a price-weighted average of 30 actively traded blue-chip stocks trading New York Stock Exchange and Nasdaq. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market. Russell 2000 is an index that measures the performance of the small-cap segment of the U.S. equity universe. MSCI International Developed measures equity market performance of large, developed markets not including the U.S. MSCI Emerging Markets (MSCI Emerging Mkts) measures equity market performance of emerging markets. Russell 1000 Growth Index measures the performance of the large- cap growth segment of the US equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). The Russell 1000 Value Index measures the performance of the large cap value segment of the US equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years). The BBB IG Spread is the Bloomberg Baa Corporate Index that measures the spread of BBB/Baa U.S. corporate bond yields over Treasuries. The HY OAS is the High Yield Option Adjusted Spread index measuring the spread of high yield bonds over Treasuries.

Sector Returns: Sectors are based on the GICS methodology. Returns are cumulative total return for stated period, including reinvestment of dividends.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC